Free State Of South Carolina St455 PDF Template

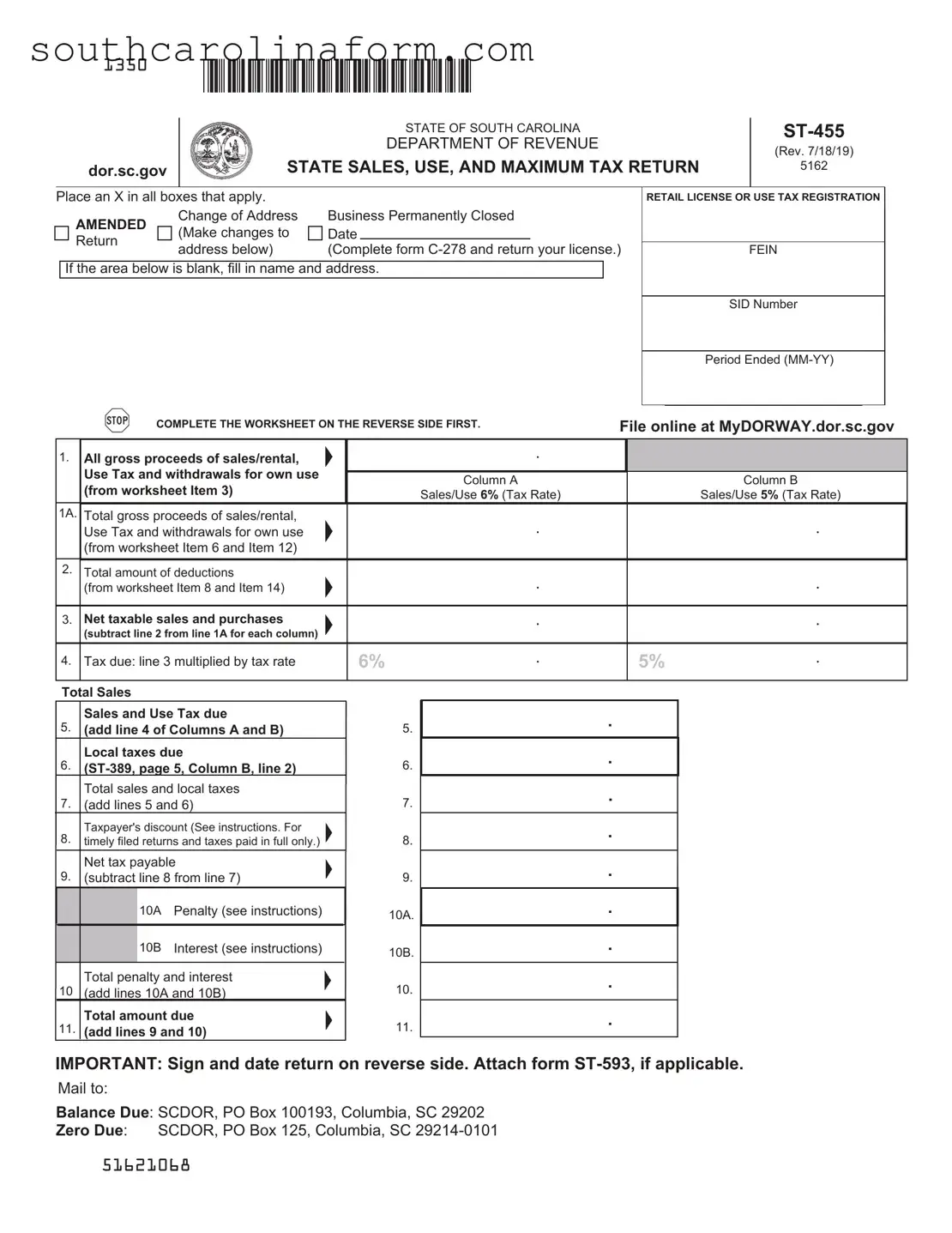

Navigating tax obligations in South Carolina requires familiarity with various forms, among which the State of South Carolina ST-455 form plays a crucial role. This document, revised last on July 18, 2019, serves as the State Sales, Use, and Maximum Tax Return, embodying essential functions for reporting and remitting sales and use taxes to the Department of Revenue. Business owners and tax preparers must mark the appropriate boxes for retail license or use tax registration, amendments, changes of address, or business closure. It's also vital for accurately filling in business details, including name, address, and FEIN or SID numbers. The form meticulously breaks down sales and use tax calculations across differing tax rates, highlighting gross proceeds, deductions, taxable sales, and the resulting taxes due. Additionally, it accounts for local taxes, taxpayer discounts for timely submissions, penalties, and interest on late payments. Detailed instructions guide the calculation process, ensuring accurate reporting. Completing and submitting this form is not only a compliance measure but also a step towards contributing to the state's fiscal health. The emphasis on details, such as the inclusion of specific tax worksheets and the requirement for attaching additional forms like the ST-389 for local taxes, underscores the comprehensive nature of this tax return. Designed to be filed both online and by mail, the ST-455 form facilitates a streamlined process for fulfilling state tax obligations, thereby supporting businesses in maintaining good standing with the State of South Carolina.

Document Preview

1350

|

|

|

|

|

|

|

|

STATE OF SOUTH CAROLINA |

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

DEPARTMENT OF REVENUE |

|

|

|

|

|

(Rev. 7/18/19) |

||

|

|

|

|

|

STATE SALES, USE, AND MAXIMUM TAX RETURN |

|

||||||||||

|

|

dor.sc.gov |

|

|

5162 |

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Place an X in all boxes that apply. |

|

|

|

|

|

|

RETAIL LICENSE OR USE TAX REGISTRATION |

|

||||||||

|

AMENDED |

Change of Address |

Business Permanently Closed |

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

||||||||

|

(Make changes to |

Date |

|

|

|

|

|

|

|

|

|

|||||

|

Return |

|

|

|

|

|

|

|

|

|

||||||

|

address below) |

|

(Complete form |

|

|

|

|

|

|

|||||||

|

|

|

|

FEIN |

|

|||||||||||

|

|

|

|

|

|

|

||||||||||

|

If the area below is blank, fill in name and address. |

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

SID Number |

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

Period Ended |

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

COMPLETE THE WORKSHEET ON THE REVERSE SIDE FIRST. |

File online at MyDORWAY.dor.sc.gov |

||||||||||||

1. |

All gross proceeds of sales/rental, |

|

|

. |

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

Use Tax and withdrawals for own use |

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

Column A |

|

|

|

|

Column B |

|||||||

|

|

(from worksheet Item 3) |

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

Sales/Use 6% (Tax Rate) |

|

|

|

|

Sales/Use 5% (Tax Rate) |

||||||

1A. |

Total gross proceeds of sales/rental, |

|

|

. |

|

|

|

|

. |

|

|

|||||

|

|

Use Tax and withdrawals for own use |

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

(from worksheet Item 6 and Item 12) |

|

|

|

|

|

|

|

|

|

|

|

|||

2. |

Total amount of deductions |

|

|

|

. |

|

|

|

|

. |

|

|

||||

|

|

(from worksheet Item 8 and Item 14) |

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

3. |

Net taxable sales and purchases |

|

|

|

. |

|

|

|

|

. |

|

|

||||

|

|

(subtract line 2 from line 1A for each column) |

|

|

|

|

|

|

|

|

|

|

|

|||

4. |

Tax due: line 3 multiplied by tax rate |

|

6% |

. |

|

5% |

. |

|

|

|||||||

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Sales

Sales and Use Tax due

5.(add line 4 of Columns A and B) Local taxes due

6.

7.(add lines 5 and 6)

Taxpayer's discount (See instructions. For

8.timely filed returns and taxes paid in full only.)

Net tax payable

9.(subtract line 8 from line 7)

|

|

10A |

Penalty (see instructions) |

|

|

10B |

Interest (see instructions) |

10 |

Total penalty and interest |

||

(add lines 10A and 10B) |

|||

11. |

Total amount due |

||

(add lines 9 and 10) |

|||

5.

6.

7.

8.

9.

10A.

10B.

10.

11.

.

.

.

.

.

.

.

.

.

IMPORTANT: Sign and date return on reverse side. Attach form

Mail to:

Balance Due: SCDOR, PO Box 100193, Columbia, SC 29202

Zero Due: SCDOR, PO Box 125, Columbia, SC

51621068

Sales and Use Tax - Worksheet #1

Item 1.

Item 2.

Item 3.

Gross proceeds of sales/rentals and withdrawals for own use |

1. |

2. |

|

Total - Gross proceeds of sales/rental, Use Tax, and withdrawals for own use |

3. |

(Add Items 1 and 2. Enter total here and on Iine 1, Column A, on front of |

|

If local tax is applicable, enter the total on ltem 1 of

Note: Sales of unprepared foods are exempt from the state Sales and Use tax rate. However, local taxes still apply to sales of unprepared foods unless the local tax law specifically exempts such sales. Sales that are subject to a local tax must be entered on the

6% Sales and Use Tax - Worksheet #2

Item 4.

Item 5. Item 6.

Item 7.

Gross proceeds of sales/rentals and withdrawals of inventory for own use |

4. |

|

(Enter sales subject to 6% tax rate requirements.) |

||

|

||

5. |

||

Total gross proceeds at 6% (Add Items 4 and 5. Enter total here and on line 1A, |

|

Column A on front of |

6. |

|

Sales and Use tax allowable deductions (Itemize by type of deduction and amount of deduction)

Type of deduction |

Amount of deduction |

a. Sales Exempt During "Sales Tax Holiday" in August |

$ |

b. Sales over $100 delivered onto Catawba Reservation |

$ |

|

$ |

|

$ |

|

$ |

|

$ |

|

$ |

Item 8. Total amount of deductions (Enter total here and on line 2 of Column A on front of |

8. |

|

< |

> |

|

Item 9. Net taxable sales and purchases (Subtract Item 8 from Item 6. Enter total here and on |

|

|

|

|

|

line 3, Column A on front of |

9. |

|

|

|

|

|

|

|

REMINDER: Form

I authorize the Director of the SCDOR or delegate to discuss this return, attachments, and related tax matters with the preparer.

Yes

No

Preparer's name |

|

Phone number |

I hereby certify that I have examined this return and to the best of my knowledge and belief it is true and accurate.

Owner, partner, or other title |

Printed name |

Taxpayer's signature |

Daytime phone number |

Date |

IMPORTANT: Your return is DELINQUENT if it is postmarked after the 20th day of the month following the close of the period. Sign and date the return.

Questions? Call

51622066

5% Sales and Use Tax - Worksheet #3

Item 10. |

Gross proceeds of sales/rentals and withdrawals for own use |

10. |

|

Item 11. |

(Enter sales subject to 5% tax rate requirements such as airplanes and boats.) |

|

|

11. |

|

||

Item 12. |

Total gross proceeds at 5% (Add Items 10 and 11. Enter total here and on line 1A, |

|

|

|

Column B on front of |

12. |

|

Item 13. |

Sales and Use Tax allowable deductions (Itemize by type of deduction and amount of deduction) |

||

|

Type of deduction |

Amount of deduction |

|

a. Sales over $100 delivered onto Catawba Reservation |

$ |

|

$ |

|

$ |

|

$ |

|

$ |

|

$ |

|

$ |

Item 14. Total amount of deductions (Enter total here and on line 2 of Column B on front of

Item 15. Net taxable sales and purchases (Subtract Item 14 from Item 12. Enter total here and on line 3, Column B on front of

14. |

< |

> |

|

|

15. |

|

|

|

|

51623064

Form Characteristics

| Fact Number | Fact Detail |

|---|---|

| 1 | The ST-455 form is a State Sales, Use, and Maximum Tax Return form used by the State of South Carolina. |

| 2 | This form was last revised on July 18, 2019. |

| 3 | The form is issued by the South Carolina Department of Revenue (SCDOR). |

| 4 | Taxpayers can file the ST-455 form online via MyDORWAY, the official filing and payment system of SCDOR. |

| 5 | The form allows for amendment declarations, including Change of Address and notification if the Business Permanently Closed. |

| 6 | It requires details of gross proceeds of sales/rentals, use tax, and withdrawals for own use to calculate the tax owed. |

| 7 | Applicable deductions are itemized in worksheets attached, guiding the taxpayer through the process of calculating net taxable sales and purchases. |

| 8 | Governing laws for the form include the state-specific tax regulations enforced by the South Carolina Department of Revenue. |

Guidelines on Filling in State Of South Carolina St455

Filling out the State of South Carolina ST-455 form is a precise task that requires attention to detail to ensure that the state sales, use, and maximum tax return are correctly reported. This process involves calculating gross proceeds, deducting sales exempt from taxes, and accurately reporting net taxable sales and purchases. By following a step-by-step approach, individuals can competently complete the form, helping to streamline their tax compliance efforts in South Carolina.

- Begin by reviewing the entire form to familiarize yourself with its requirements and identify all the sections you need to complete, based on your business transactions.

- Place an "X" in the applicable boxes at the top of the form to indicate whether it’s a regular return, an amended return, a change of address, or if the business has permanently closed.

- If the area for your business name and address is blank, fill in the relevant information accurately to ensure your return is properly processed.

- Locate the worksheets on the reverse side of the form to calculate the figures required for the form's front side. Begin with Worksheet #1 for 6% sales and use tax calculations.

- Enter the total gross proceeds of sales/rentals and withdrawals for own use in Item 3 of Worksheet #1, calculating the sum of Items 1 and 2.

- For sales subject to a 5% tax rate, such as airplanes and boats, use Worksheet #3 to calculate gross proceeds (Item 12) by adding Items 10 and 11.

- Calculate and enter the total amount of deductions for both tax rates in Item 8 of Worksheet #1 for 6% rate deductions and Item 14 of Worksheet #3 for 5% rate deductions.

- Subtract the total deductions from the total gross proceeds to get the net taxable sales and purchases for each tax rate. Enter these totals in Item 9 of Worksheet #1 and Item 15 of Worksheet #3, respectively.

- Transfer the calculated totals to the front of the ST-455 form, filling in lines 1A, 2, and 3 for both Column A (6% tax rate) and Column B (5% tax rate) accordingly.

- Multiply the net taxable sales and purchases by the tax rate (6% or 5%) to calculate the tax due for each column, and enter these amounts in lines 4 of Columns A and B.

- Add the tax due for both columns to calculate the total sales and use tax due, entering this sum in line 5.

- If local taxes are due, complete form ST-389, entering the total local taxes due in line 6 of the ST-455 form.

- Add the total sales and local taxes due to get the total sales and local taxes figure, and enter it in line 7.

- Calculate any applicable taxpayer's discount for timely filed returns and enter this amount in line 8, then subtract it from the total sales and local taxes to find the net tax payable, which should be entered in line 9.

- Consult the instructions to calculate any penalty and interest due, entering these amounts in lines 10A, 10B, and the total of these in line 10.

- Add lines 9 and 10 to find the total amount due and enter this in line 11.

- Sign and date the return, ensuring that all required attachments, such as form ST-593 if applicable, are included.

- Review the entire form to ensure all necessary information has been accurately provided and submit it to the appropriate address, depending on whether there is a balance due or not.

Upon completing and submitting the State of South Carolina ST-455 form, individuals fulfill their responsibility in reporting sales, use, and maximum taxes. Careful adherence to the instructions and accurately provided information ensures compliance with state tax laws, thus avoiding potential penalties and ensuring the smooth operation of one's business within the legal frameworks of South Carolina.

Common Questions

What is the State of South Carolina ST-455 form used for?

The State of South Carolina ST-455 form is utilized for reporting state sales, use, and maximum tax. This form allows businesses to declare their gross proceeds from sales or rentals, use tax, and any withdrawals for their own use, thereby calculating the amount of tax owed to the Department of Revenue. It plays a crucial role in ensuring businesses comply with state tax regulations.

Can I file the ST-455 form online?

Yes, the ST-455 form can be filed online through South Carolina's Department of Revenue website, MyDORWAY. This online platform simplifies the filing process, making it easier, faster, and more secure for taxpayers to submit their sales, use, and maximum tax returns directly to the state.

What should I do if I need to amend my ST-455 form?

If you discover that your initial ST-455 submission contained errors or was incomplete, you can file an amended return. To do so, you should mark the 'AMENDED' checkbox on the form, correct the information, and submit it again. Keep in mind that providing accurate and complete information is essential to avoid potential penalties or additional assessments.

What happens if my business permanently closes?

If your business permanently closes, you are required to indicate this on the ST-455 form by marking the relevant checkbox. Additionally, complete form C-278 and return your sales tax license to the South Carolina Department of Revenue. It's important to finalize all tax obligations to ensure your business is properly closed in the eyes of the state.

How do I calculate the tax due on the ST-455 form?

To calculate the tax due, start by completing the worksheet on the reverse side of the ST-455 form. This includes determining your gross proceeds of sales/rentals and withdrawing for own use, subtracting allowable deductions, and calculating net taxable sales and purchases. Multiply your net taxable amount by the applicable tax rate(s) provided on the form to determine the tax due. Additionally, ensure to factor in local taxes and any taxpayer discounts for timely filed returns.

Is it possible to receive a discount for timely filing the ST-455 form?

South Carolina offers a timely filing discount to taxpayers who submit their ST-455 form and full payment by the deadline. This discount is calculated based on the total sales and use tax amount due. To qualify, ensure your return is filed and the tax due is paid by the 20th day of the month following the close of the tax period. Check the specific terms on the form instructions or the Department of Revenue website for the exact discount rate and qualification criteria.

Common mistakes

Not marking the applicable boxes at the beginning of the State of South Carolina ST-455 form is a common error. This oversight can include failing to indicate if the form is an amended return, if there’s been a change of address, or if the business has permanently closed. Such details are crucial for accurate processing.

Incorrectly reporting gross proceeds on the worksheets on the reverse side of the form can lead to substantial errors in tax calculation. This typically happens when individuals either misinterpret what constitutes gross proceeds of sales/rentals and withdrawals for own use or simply input incorrect figures.

Failing to include deductions in the total amount on the worksheets is another frequent mistake. Taxpayers might overlook or miscalculate eligible deductions, such as sales exempt during the "Sales Tax Holiday" or sales over $100 delivered onto the Catawba Reservation, which can affect the net tax payable.

Omitting to calculate and include the tax due accurately. After deducing the eligible amounts, the next step is to apply the correct tax rates (6% and 5%) to the net taxable sales and purchases. Errors in this calculation can either inflate or understate the total sales and use tax due.

Incorrectly filling out local taxes due and omitting form ST-389 where applicable. Local taxes require careful attention to ensure all applicable sales that are subject to local tax are correctly reported. Forgetting to attach form ST-389 can result in incomplete filing if local taxes are relevant to the taxpayer’s sales.

Avoiding these mistakes ensures a smoother process in filing the State of South Carolina ST-455 form. Double-checking all sections, ensuring accurate calculations, and paying attention to details can help taxpayers avoid unnecessary errors and potential penalties.

Documents used along the form

When businesses file the State of South Carolina ST-455 form for state sales, use, and maximum tax returns, several other documents often accompany this filing to ensure compliance and accuracy. Understanding these documents is key to navigating the state's tax regulations effectively.

- ST-389: Local Taxes Worksheet - This form is essential for reporting and calculating any local taxes that may be due in addition to state sales and use taxes. It covers various local jurisdictions and ensures taxes are accurately allocated according to where sales occur.

- SC1040: South Carolina Individual Income Tax Return - Sole proprietors or individuals in a partnership may need to attach this form if their personal income is affected by the business's profits and losses reported on the ST-455.

- C-278: Closing Business Form - For businesses that are permanently closing, this form must be submitted along with the ST-455 to notify the Department of Revenue of the closure and ensure that all final tax liabilities are settled.

- ST-593: Sales and Use Tax Exemption Certificate - Used by exempt organizations or in transactions where sales tax should not be collected, this certificate must be filed with the ST-455 when claiming exemptions on taxable sales.

- UT-3: Use Tax Return - For transactions that do not involve sales but are still subject to use tax, this form is necessary. It allows businesses to report and pay use taxes on out-of-state purchases, equipment, and other taxable items used in the business.

These documents play a pivotal role in fulfilling tax obligations in South Carolina. By accurately completing and submitting these forms alongside the ST-455, businesses can ensure compliance with state tax laws, avoid penalties, and maintain good standing with the Department of Revenue. It's crucial for business owners and tax professionals to familiarize themselves with these forms to navigate the tax filing process smoothly.

Similar forms

The State of South Carolina ST-455 form, designed for the calculation and reporting of state sales, use, and maximum taxes, bears resemblance to a variety of other tax-related documents tailored to distinct purposes or jurisdictions. One such document is the State of North Carolina E-500, which serves as the Sales and Use Tax Return. Both forms share the intrinsic goal of collecting tax owed on sales, rentals, and purchases made within the respective states. They require detailed information about gross sales, applicable deductions, and the net taxable amount, structuring this data to facilitate accurate tax calculation and compliance with state laws.

Similar yet not identical, the California State Board of Equalization's Sales and Use Tax Return mirrors the South Carolina ST-445 form in function and intent. Offering a platform for businesses to report and remit taxes on sales and purchases, this document emphasizes the importance of understanding local jurisdictional tax rates, much like the ST-455's attention to distinctions between general and specific taxable items. California's form additionally mandates information on district taxes, echoing the complexity faced by filers of the ST-455 grappling with local taxes due.

The New York State Department of Taxation and Finance's ST-810 form, utilized for quarterly sales and use tax filings by vendors, aligns with the ST-455's structure regarding the reporting of gross sales, deductions, and net taxes due. Both documents underscore the critical nature of timely, accurate tax reporting for businesses, ensuring municipal and state governments receive necessary revenues to fund public services. The emphasis on detail, accounting for taxable and exempt transactions, showcases the documents’ roles in maintaining tax system integrity.

Florida's Discretionary Sales Surtax Information (Form DR-15DSS), although focusing primarily on the surtax aspect, complements the essence of South Carolina's ST-455 by addressing sales and use tax obligations at a more localized level. It highlights the variations in tax rates across counties, akin to the ST-455's accommodation for local tax calculations. Each form educates filers on jurisdiction-specific requirements, guiding businesses through the nuanced landscape of state and local taxation.

Similarly, the Texas Sales and Use Tax Return (Form 01-114) provides a comprehensive framework for reporting state, city, county, and special jurisdiction taxes, akin to the multifaceted approach of the ST-455. Both forms expect businesses to dissect their sales and transactions meticulously, applying different tax rates where applicable to comply with a layered tax structure. This detailed reporting ensures accurate allocation of tax revenues to various governing entities.

Another counterpart is the Illinois Sales and Use Tax Return (Form ST-1), dedicated to capturing a wide array of taxable transactions within the state. Like the ST-455, it requests detailed breakdowns of sales, deductions, and taxes due, catering to a broad spectrum of sales and use tax scenarios. Both documents facilitate the state's efforts to collect taxes effectively, thereby supporting essential public services, from infrastructure to education.

The Ohio Sales and Use Tax Return (Form UST-1) demonstrates another example of a state-specific approach to tax collection, mirroring the ST-455’s comprehensive nature. It outlines the necessity for businesses to calculate and report taxes accrued from sales and services, adjusting for various exemptions and tax brackets. This form, akin to South Carolina's, serves as a crucial tool in upholding the state's fiscal responsibilities.

Pennsylvania's Sales and Use Tax Return (PA-3) shares the objective of detailing transactions subject to sales and use taxes. It mandates the accounting of taxable sales, permissible deductions, and the calculation of net taxes in a manner that parallels the ST-455. The emphasis on accurate, detailed reporting underscores both forms' roles in ensuring compliance with state tax laws and supporting government operations through generated revenues.

Michigan's Sales, Use, and Withholding Taxes Monthly/Quarterly Return (Form 5080), although encompassing withholding taxes in addition to sales and use taxes, presents a comprehensive approach similar to the ST-455. By requiring detailed transactional data and accommodating various tax rates, it ensures businesses contribute correctly to state coffers. This multipurpose nature reflects the complex landscape of state tax administration.

Lastly, the Virginia Sales and Use Tax Return (Form ST-9) offers a close comparison in its requirement for sellers to report gross sales, deductions, and calculate taxes due. Both this form and the ST-455 guide businesses through the nuances of tax compliance, highlighting exempt sales and the impact of local tax rates. Through this detailed reporting, both forms play a vital role in sustaining public services via tax revenue.

Dos and Don'ts

When preparing the State of South Carolina ST-455 form, it is crucial to follow certain guidelines to ensure the process is completed correctly. Below are four dos and don'ts that can help streamline the process and avoid common pitfalls.

Dos:- Ensure all applicable boxes at the top of the form, such as "Amended," "Change of Address," or "Business Permanently Closed," are checked accurately to reflect the current status.

- Complete the worksheet on the reverse side first, as it provides the detailed calculations needed to fill out the main form correctly.

- File online at MyDORWAY.dor.sc.gov if possible, for a more streamlined and efficient filing process.

- Sign and date the return on the reverse side to verify the accuracy and authenticity of the information provided.

- Do not leave the gross proceeds, deductions, or net taxable sales and purchases sections blank. Ensure every field is completed with accurate information.

- Avoid guessing or estimating figures. Use actual sales data and accurate calculations to determine the amounts to be reported.

- Forget to attach Form ST-593, if applicable. This form is necessary for certain types of sales and must accompany the ST-455 when required.

- Miss the filing deadline. Remember, your return is considered delinquent if it is postmarked after the 20th day of the month following the close of the reporting period.

Misconceptions

One common misconception is that the ST-455 form is only for businesses selling physical goods in South Carolina. In reality, this form also applies to businesses providing taxable services, renting out property, or even those making use of goods within the company (withdrawals for own use).

Many believe that all sales are taxed at the same rate. However, the ST-455 form clearly distinguishes between different tax rates: 6% for general sales/use and 5% for specific items like airplanes and boats, showcasing the varying tax rates applicable under different circumstances.

There’s a misconception that online filing is an option, not a requirement. While the form indicates the capability to file online via MyDORWAY.dor.sc.gov, the South Carolina Department of Revenue strongly encourages online filing for efficiency and quicker processing times.

Some assume that if they are out of state, they don't need to file the ST-455. However, out-of-state purchases subject to use tax require filing if the items are used, consumed, or stored in South Carolina, highlighting the tax’s scope beyond the physical boundaries of the state.

Another misconception is that sales made to other businesses for resale are automatically exempt from sales tax. Although there are exemptions, such sales require proper documentation and aren’t exempt by default. Businesses must maintain records of exemption certificates to prove the tax-exempt nature of these transactions.

Many people mistakenly believe that late filing only results in minor penalties. The form outlines specific penalties and interest for late filings, which can accumulate significantly over time, emphasizing the importance of timely compliance.

There is also confusion about the taxpayer's discount mentioned in the instructions. Some interpret this as a discount on the goods sold, whereas it's actually an incentive for timely filing and tax payment, calculated as a percentage of the tax due.

A common misconception is that once you file and pay taxes using the ST-455, there are no additional steps. However, Form ST-389 (for local taxes) must also be completed and attached if applicable, highlighting the layered nature of tax compliance in South Carolina.

Some believe the ST-455 covers all state and federal tax obligations. This form is specifically for state sales, use, and maximum tax returns in South Carolina. Businesses have separate obligations for federal taxes and other state taxes beyond those covered by the ST-455.

Many first-time filers think that the ST-455 is too complex to complete without professional help. While seeking guidance can be beneficial, the form, along with its instructions and worksheets, is designed to be manageable for anyone to complete, as long as careful attention is paid to the details and instructions.

Key takeaways

Filling out and using the State of South Carolina ST-455 form requires attention to detail and an understanding of the sales, use, and maximum tax reporting process. Here are some key takeaways to aid individuals and businesses in accurately completing the form:

- The ST-455 form is used for reporting gross proceeds from sales or rentals, use tax, and withdrawals for one's own use.

- To ensure accuracy, complete the worksheet on the reverse side of the form before filling out the main portion.

- Filers need to specify if the return is an amended version, involves a change of address, or if the business has permanently closed by marking the appropriate box at the top of the form.

- It is crucial to report the gross proceeds of sales or rentals and withdrawals for own use, separating them by tax rate categories (6% and 5%) as indicated in the form.

- Deductions allowable under the sales and use tax law should be clearly itemized and reported to reduce gross sales to net taxable sales and purchases.

- Local taxes due on sales must be calculated and reported separately on form ST-389, which is attached to the ST-455.

- Taxpayers are eligible for a discount if the return is filed timely and the taxes are paid in full. This discount must be calculated and subtracted to find the net tax payable.

- Penalties and interest apply for late filings and payments, and these should be calculated as instructed and added to the total amount due.

- The form must be signed and dated on the reverse side. If a tax preparer completed the form, their contact information and authorization to discuss the return with the Department of Revenue should be provided.

- The completed form should be mailed to the appropriate address, depending on whether a balance is due or not. It’s important to ensure it is postmarked by the 20th day of the month following the close of the reporting period to avoid penalties.

Accurately completing and promptly submitting the ST-455 can help businesses remain compliant with South Carolina’s tax obligations, avoid penalties, and benefit from applicable discounts for timely filing and payment.

More PDF Templates

Do You Need a Fishing License in South Carolina - The process outlined by the form demonstrates a balance between regulatory requirements and the facilitation of access to recreational licenses for the disabled population.

Certificate of Vaccination - Assists in maintaining a safe and healthy environment for all children in SC day cares and schools.

South Carolina Retirement - Members have the option to revoke previous beneficiary designations, ensuring up-to-date choices are honored.